Related Articles

What Is Health Insurance?

Health insurance is a type of insurance that covers medical expenses incurred on an illnessor injury. These medical expenses include…

Read More

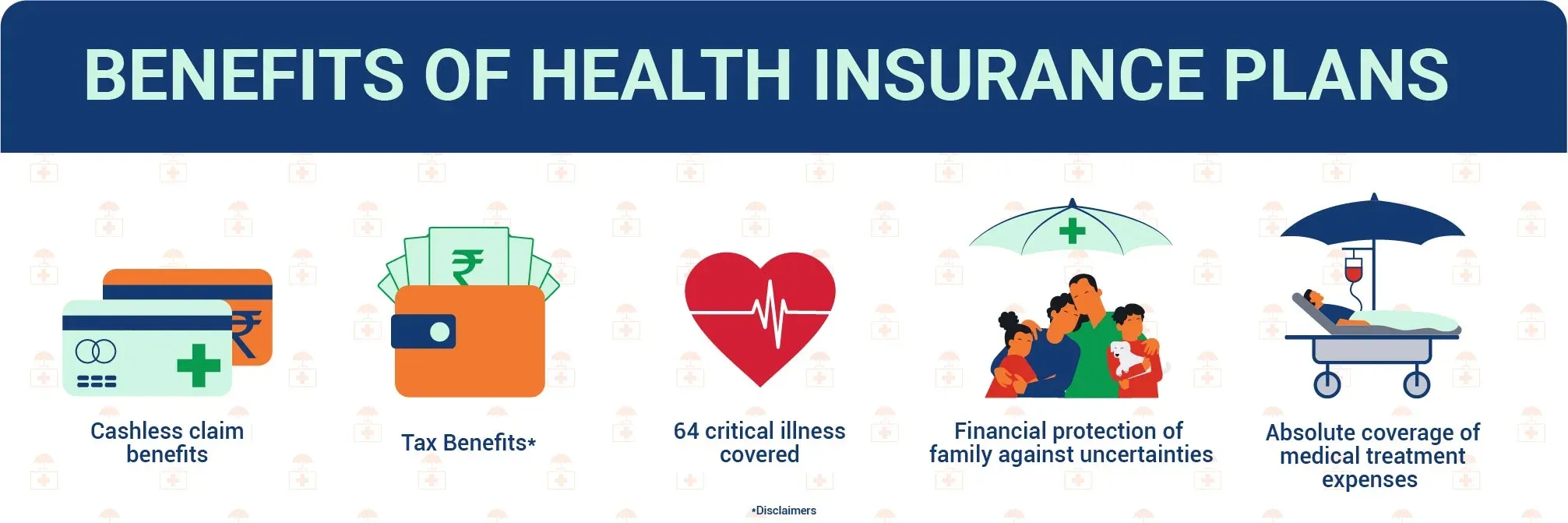

Benefits of Health Insurance

Health issues have become an increasingly pressing concern in the past few years. The average persons lifestyle today involves greater…

Read More

What is Mediclaim?

if this is one of the questions that is keeping you from getting comprehensive financial security for your health, then we are here to help…

Read More

We would like to hear from you

Let us know about your experience or any feedback that might help us serve you better in future.

Do you have any thoughts you’d like to share?