Related Articles

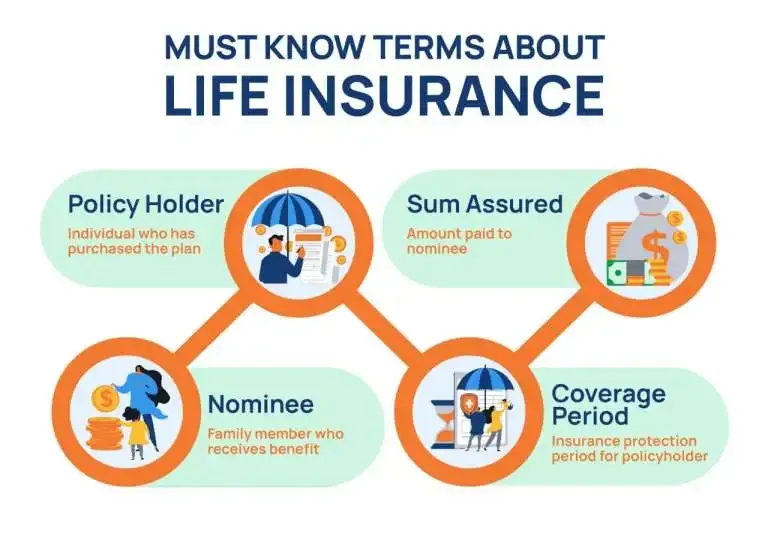

What is Life Insurance Policy?

What is life insurance meaning, you should know that a life insurance policy is a contract between an individual and an insurance provider, in which the insurance company gives financial protection…

Read More

Benefits of Life Insurance

We live a life full of uncertainties. In today's world, financial security is crucial to living a stress-free and peaceful life. It is critical to protect your loved ones from unforeseen circumstances…

Read More

Advantages of Buying Life Insurance Plan at Early Age

According to a study conducted by the IRIS Knowledge Foundation and UN-Habitat, the population in the 15-34 age group is steadily rising in India. It stood at 353 million in 2001 and rose to 430 million in 2011…

Read More