Related Articles

What is Life Insurance?

Life insurance can be defined as a type of insurance scheme that makes a payment to a specific beneficiary or group of beneficiaries in the case of the policyholder’s demise.....

Read More

Types Of Life Insurance Policies in India

Choosing from the different types of life insurance in India is a crucial financial decision, as it helps you protect your loved ones from life’s uncertainties. Still, you may not be fully aware of the types of life insurance policy in India and how they....

Read More

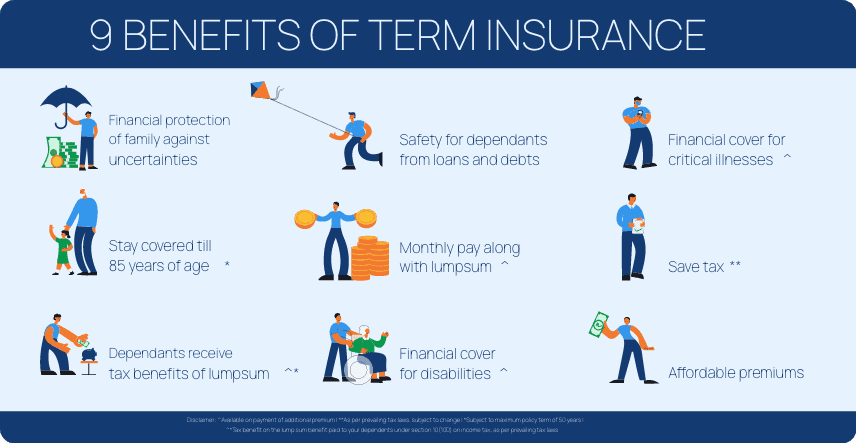

Term Insurance

Term insurance is the simplest and purest form of life insurance, offering financial coverage to the policyholder against fixed premiums for a specified duration – hence the name ‘term’....

Read More